How to Manufacture a Local Stablecoin

A field guide to building touchable money

What happens to the local economy when everyone saves and trades in USD?

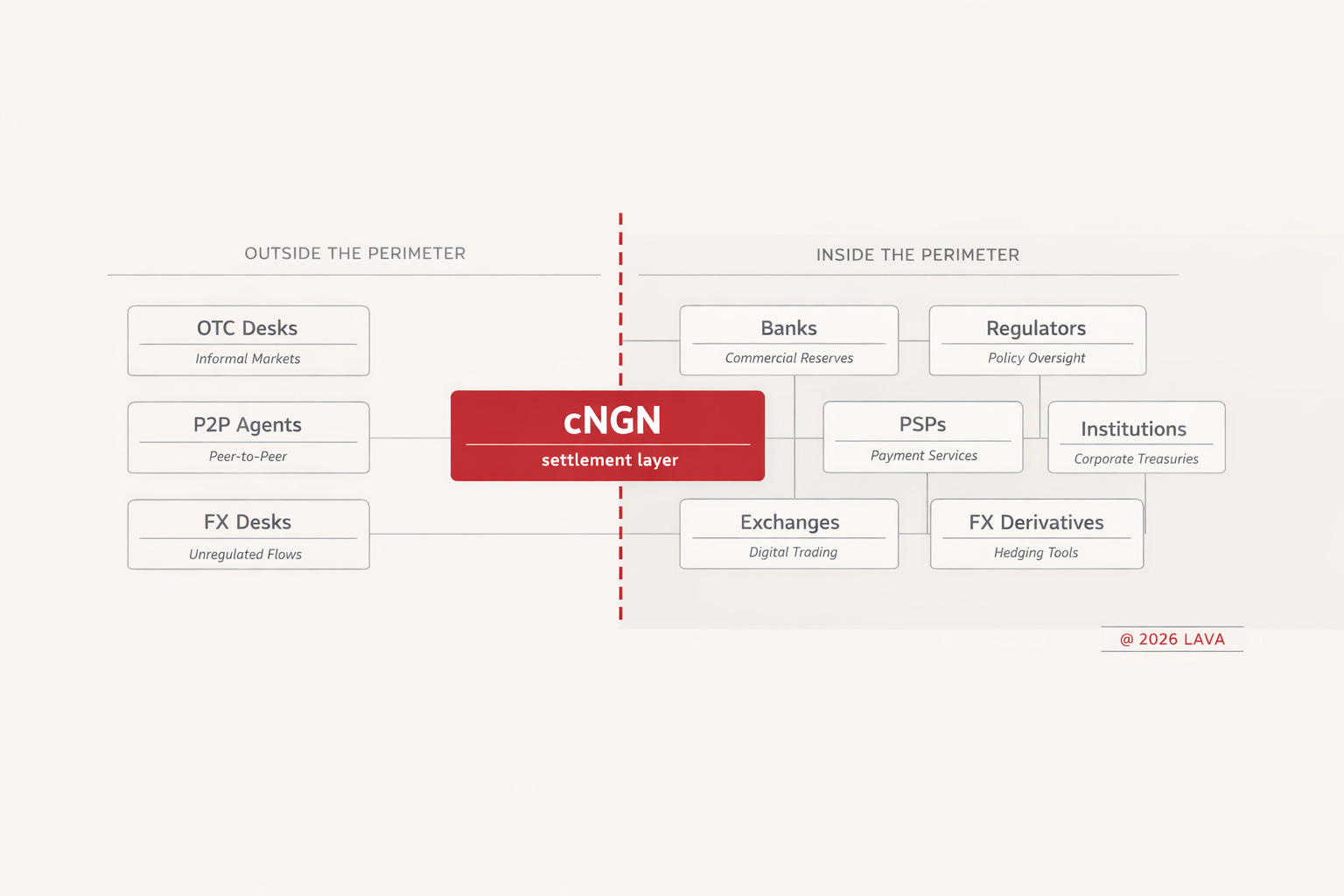

The Libra/Diem saga showed us one thing: sovereign states will not sit by and watch people and businesses route around the local financial system in a way that makes local policy powerless. To preserve fiscal sovereignty, they lock all unseen money out of the Currency Perimeter; the boundary of rules that determines what regulated entities are allowed to treat as money, where it clears, when it settles, and when it is permitted to exit into a harder unit of account.

If the perimeter doesn’t admit it, it won’t become infrastructure.

But liquidity is like water. It finds the path of least resistance. In 2021, the Nigerian government turned crypto into a landmine for institutions. The command to institutions was clear; you cannot touch crypto. So the market routed around them. Importers, treasurers, and consumers moved onto the Shadow Rail: OTC desks, WhatsApp agents, and informal coordination layers that were riskier, less legible, and harder to control, but still preferable to getting trapped inside the formal system.

Regulators quickly realized the perimeter was leaking. They saw USD stablecoins becoming the de facto unit of account. The state’s first response was the eNaira—a defensive attempt to regain visibility and control through a state-backed digital currency. It failed because it had no differentiated interest, no additional FX access, running on a permissioned chain that offered users nothing the naira couldn’t already do. But a less-obvious reason why it failed was that the CBN tried to build consumer distribution from scratch, bypassing the fintechs and payment companies that had spent decades figuring out how to reach Nigerians where they actually are. The result was a ghost town: a year after launch, 98.5% of wallets had not been used even once in a given week despite being the second-largest CBDC project in the world.

The eNaira was a failure, but it was also a signal. It showed that the powers that be understood the power of digital currency and still refused to surrender the perimeter. More importantly, it revealed the form a local stablecoin would need to take to be admitted: digitally native enough to modernize the system, yet legible enough to leave power anchored in the local economy.

cNGN is that middle ground.

Between the regulator and the market

People in African fintech like to name-drop and claim to be “close to regulators.” Usually, it means someone in the CBN is their mutual on X, or they shared a panel three Africa Fintech Summits ago. While others are collecting business cards like infinity stones, Convexity, the team behind cNGN, are active contributors to policy discussions.

Deji, co-founder of cNGN, is the kind of person the powers call on when something goes wrong that they don’t fully understand. As co-founder of A&D Forensics and Chainalysis’s sole investigative partner across Africa, he spent years in the sewage of financial crime: training officials of the Economic and Financial Crimes Commission on crypto investigation, working with Zambia’s Financial Intelligence Unit, helping the Nigerian Army’s CyberWarfare command understand “what is this blockchain thing.” He helped shape the IVMS101 messaging standard that global crypto AML runs on. When the SEC needed to draft Nigeria’s virtual asset regulatory framework, Deji was in the room. He’s not your average crypto bro — high on hype. Deji’s real power is an obsession with the boring parts that others are too impatient to acknowledge, let alone try to fix.

Uyoyo, another co-founder of cNGN, is a lawyer by training—banking, corporate, and securities law—who moved through asset management and an investment fund before arriving at Convexity. Before cNGN, he led CHATS.Cash, a humanitarian aid distribution platform designed to cover hard-to-reach places. Additionally, he co-led a project that the CBN and Ministry of Humanitarian Affairs contracted Convexity to build, ensuring donor funds reached beneficiaries in low-income communities onchain. That work put him in direct relationship with the CBN for a product that had nothing to do with stablecoins. He walked into cNGN with relationships already earned.

Charles, co-founder of Convexity and founding architect of cNGN, spent years as a blockchain solutions architect—including work with Sterling Bank—which gave him an early view into exactly how traditional financial institutions think about blockchain risk before they’ll touch it. He is the builder underneath everything Deji and Uyoyo take into regulatory conversations.

When cNGN applied for its SEC Approval-in-Principle under the Regulatory Incubation Program, the team had spent years helping regulators solve their hardest problems. In markets where the perimeter is enforced by humans, that depth of relationship is the only currency that matters.

What they built

cNGN is a locally pegged settlement instrument that lives on public rails while remaining redeemable into local banking money. It is designed to sit inside the Currency Perimeter, making it touchable for regulated balance sheets. Launched in February 2025, it already reports roughly ₦2.5 billion in circulation.

It is not just a token that mirrors the price of legal tender. cNGN combines the approvals, controls, redemption paths, and operational discipline that make a local digital unit usable under scrutiny:

infrastructure that makes the naira programmable and compatible with digital rails

an approval path that gives counterparties a defensible reason to touch it

onchain forensics and incident response posture that reduces regulatory fear

redemption and oversight processes that can be explained under pressure

In Nigeria, compliance is more than a checklist, it is a set of relationships and escalation paths. When things break, somebody has to pick up the phone. Convexity has been that somebody for years.

When a business moves into USD₮, they are draining the local system. When they move into cNGN, they are strengthening it. Because cNGN is an onshore asset with reserves sitting in Nigerian commercial banks and local T-bills, it allows institutions to participate in the digital economy without triggering capital flight.

The obvious objection is that a locally pegged stablecoin doesn’t eliminate the incentive to flee to harder currencies; it just makes the exit more convenient. cNGN doesn’t try to reverse that incentive. What it offers instead is a cleaner way to move through the NGN side of that trade. Compared with informal OTC channels, it gives businesses and fintechs an onshore, auditable, and easier-to-reconcile settlement rail—one that does not depend on after-hours coordination, fragile trust networks, or stepping outside the perimeter. Its role is not to stop demand for harder currencies. It is to make digital NGN usable in a form regulated actors can hold, settle with, and defend. For a full case on why dollarization matters and what’s at stake, read our earlier piece here.

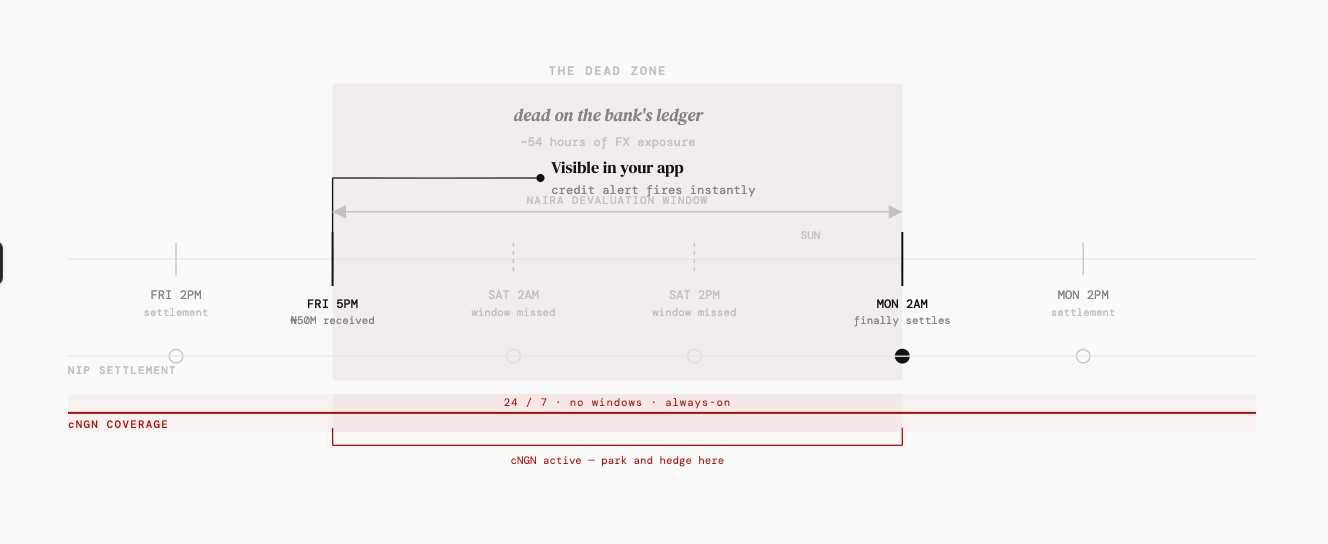

Schrödinger’s Payment

Picture this: It’s Friday evening, and you receive a payment of ₦50M. The credit alert pings, and the number shows up in your app—except it’s not really there. Nigeria’s Instant Payment system is a Deferred Net Settlement system, which means that actual settlement between banks only happens within specific windows—2:00 AM and 2:00 PM daily. The money sits in limbo: visible in the app, but dead on the bank’s ledger until the next window opens. In an economy where prices swing before you can get a response back for “what’s the dollar rate?” Twelve hours of holding the wrong currency is a very serious risk.

This creates two needs that the Shadow Rail previously monopolized;

After-hours settlement: the structural need for institutions to reconcile and move value when the formal windows are shut; and

Overnight hedging: the strategic need for merchants to move funds to avoid waking up to a devaluation on Monday morning.

cNGN provides a touchable answer to both. Because it is 1:1 backed and SEC-allowed, it functions as a 24/7 vault that businesses can justify holding. Businesses pay for that hedge because the alternative is bearing FX risk overnight.

The market is already responding. Uyoyo estimates that 70–80% of circulating cNGN is actively moving, used for treasury parking and settling trades. What’s more telling is the shape of the movement: small and mid-sized wallets represent over 95% of holding addresses, with the smallest wallet cohort making up 75.2% of addresses. This shows broad participation and repeat distribution, not a small cluster of whale wallets moving massive blocks of capital once a month. Money behaving like money.

For institutions, cNGN offers a settlement leg that stays usable outside banking hours, is traceable end-to-end, and doesn’t require a phone call to reconcile. “Cross-border” here doesn’t mean replacing correspondent banking. It means cleaning up the NGN leg—the part that usually gets messy at the edges.

For consumers, the value proposition is simple: fewer “will this work?” moments thanks to always-on NGN settlement that doesn’t inherit bank constraints, lower-friction NGN legs for apps routing stablecoin flows, and more defensible last-mile rails for merchants who need NGN exposure without living inside informal coordination.

For the Naira to catch up to the internet, it had to become programmable. cNGN is the shape of that adaptation.

Nigeria is hard mode proof

Nigeria is hard mode. Volatile currency, a shadow economy moving billions the formal system can’t see, and regulators whose default answer is no (and whose second answer is also no). If you can crack the perimeter here, you can crack it anywhere. cNGN cracked it, and in doing so created proof that it can be done—and a map for how. Across Africa, the problem repeats: different central banks, different political constraints. Yet, it’s the same shape of demand, the same potential upside if it works.

The code ports easily. Every team building a local stablecoin knows this. The difficult part—that most teams overlook—is everything else: the years of relationship-building, the compliance grunt work, the explaining and explaining again. Getting the actors who control the perimeter to align around one instrument requires trust that cannot be rushed and coordination that cannot be shortcut.. There is no alternative path to the same outcome, and there is no faking admission into the perimeter. That’s where most local stablecoin attempts die. Coordination is the moat, and regulatory credibility is what makes coordination possible. Convexity spent a decade earning both before cNGN was even a conversation.

Where this breaks—or compounds

We made a bet that cNGN will do well over the long run, yet it’s too early in the game to tell if it is a clear winner. To become true infrastructure, it must clear three constraints that every touchable settlement instrument eventually runs into.

Liquidity cold start: liquidity depth beats coverage early. The tell is whether liquidity consolidates in defensible venues with tight spreads, so cNGN can graduate from “available” to “referenceable.”

Operational reliability: institutions keep routing through an asset only if redemption, reconciliation, and incident response stay predictable under stress. If that trust breaks once, institutions won’t come back.

Dollar gravity: USD will likely remain the de facto store of value in volatile economies. The worry for any local stablecoin is that it becomes merely a bridge to USD—a unit nobody wants to hold, only pass through. cNGN doesn’t fight that gravity, nor does it need to. Whether people park overnight value in USD, tokenised gold, or something else entirely, they still need to exit and re-enter NGN at some point. That crossing point—fiat in, fiat out, clean and auditable—is where cNGN lives. It works both ways: stronger domestic settlement, and a faster path into harder currency when that’s where people are headed anyway. The settlement layer stays the same regardless of what sits above it.

We backed cNGN because it addresses the problem nobody else wanted to solve: the point at which institutions decide what counts as money and regulators decide what they can tolerate. If the handshake holds, the Naira becomes a settlement API—always-on, auditable, and easily reconcilable.

The long-term implication is larger than Nigeria. If this works, African economies can show up as themselves and participate in digital commerce without having to borrow someone else’s currency.

By making the unit touchable, cNGN can be three things at once: fast enough for the internet, constrained enough for the state, and liquid enough for the market to treat as real money.

where does NGNT feature in this timeline/analysis?