What Is Tokenisation Actually Good For?

Most of what you're being sold about tokenization is snake oil. Here's the version we'd actually invest in — and what it looks like in Africa.

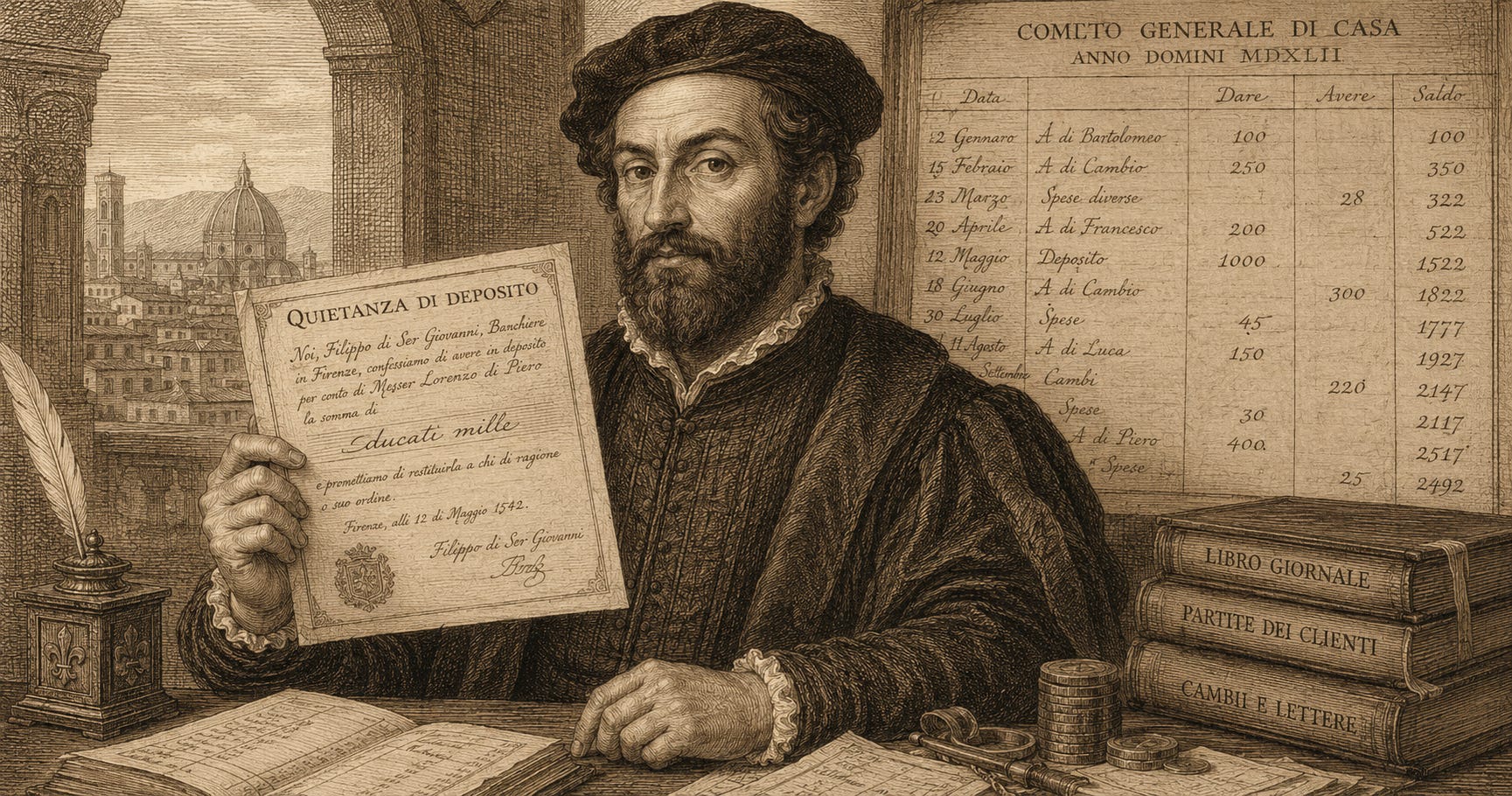

Tokenization is not new. In 1564, a bright spark in Italy got tired of withdrawing silver from a bank vault every time they wanted to trade, so they issued fede di deposito (a.k.a. tokenized silver) and let those circulate instead. Negotiable certificates of deposit, repos, T-bills, ETFs: most modern money-market instruments are already tokens. We just don’t call them that.

So when people sell you “tokenization” as a new asset class, they’re really selling you a new medium. Most of what’s loaded onto that pitch (“access”, “democratization”, “real-world assets onchain”) is, in our view, snake oil. There is one thing the medium does that the old one couldn’t, and getting that one thing right is at the heart of what we think is investable.

In the full piece we argue:

Why “access” is a useful word only when it changes what kind of liquidity enters a market.

Why the genuine advantage of a public ledger as a medium is atomic delivery vs payment without a central counterparty and what that actually unlocks.

Why permissioned token standards (ERC-3643, Canton) are ironic, and end up fragmenting liquidity rather than freeing it.

Why derivatives, not ownership, are where tokenization actually shines, and how HIP-3 and HIP-4 open this up for African builders to discover their own prices.

What we will and won’t back at LAVA: principled derivatives over jurisdiction-licensed RWAs.

Read the full piece here → A Token of Truth