Stablecoins in Africa (Part I)

How USD Stablecoins Became Core Financial Infrastructure

More than 90% of Nigeria’s USD liquidity flows outside the banking system, according to the Nigerian Forex Bureau Association. This isn’t a bug - it’s a feature of major African economies.

Today, USD stablecoins have become the primary coordination mechanism for this massive parallel USD economy.

The story isn't that Africans use stablecoins instead of banks. The story is that stablecoins finally solved Africa's decades-old USD coordination problem, in and out of the banking system. If you're a major energy company, import/export business in Africa, or even Starlink, you're more likely to access USD for your day-to-day operations through stablecoins than through banks.

USD stablecoins make up 43% of all recorded onchain transactions in Africa (2024). While USD stablecoins became popular in the West more recently, Africa has been a pioneer in leveraging stablecoins as core plumbing for global trade, payments, and treasury management.

Why did Africa become the testing ground for this financial revolution?

Three converging forces created the perfect storm: chronic USD scarcity in banking systems, fragmented parallel USD markets, and widespread mobile money infrastructure. The result? $50B of USD Stablecoin transactions that are faster and cheaper than traditional banking or informal Forex services. Beyond the numbers, how embedded USD stablecoins have become is a powerful indicator of where we are headed.

Africa’s USD crisis created a large parallel economy

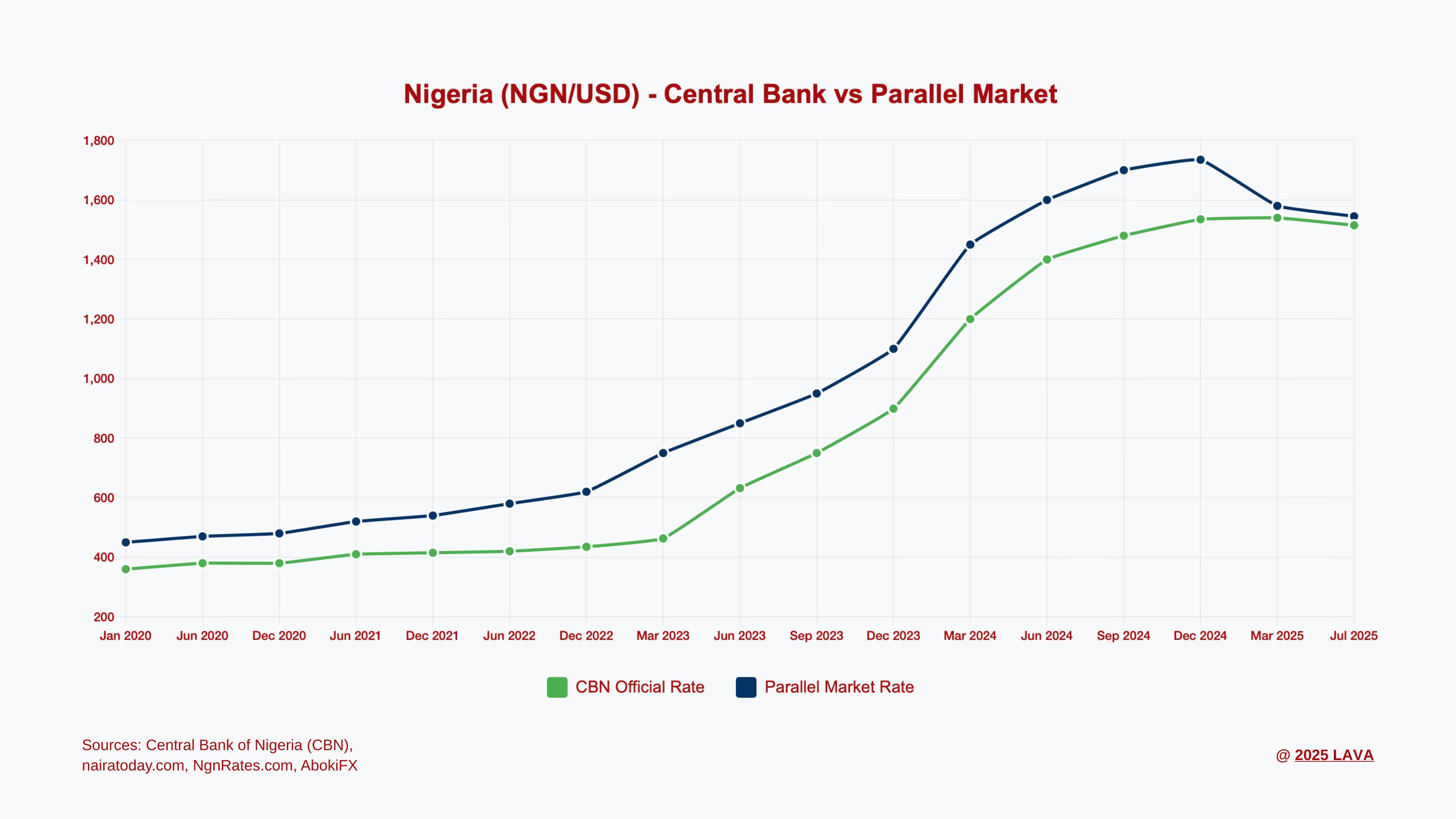

Nigeria - Africa's most populated country - saw major banks suspend USD transactions with their debit cards for 3-years (starting 2022). Customers would buy USD in parallel markets, then deposit it for the privilege of spending through official channels - including to keep their Google and Microsoft subscriptions, travel, and transact in the internet economy. Even when restrictions eased, limits remained at just $500/month - $1000/quarter and $20 a day. Furthermore, foreign airlines operating in Nigeria were owed over $700M due to matured foreign exchange obligations (2024).

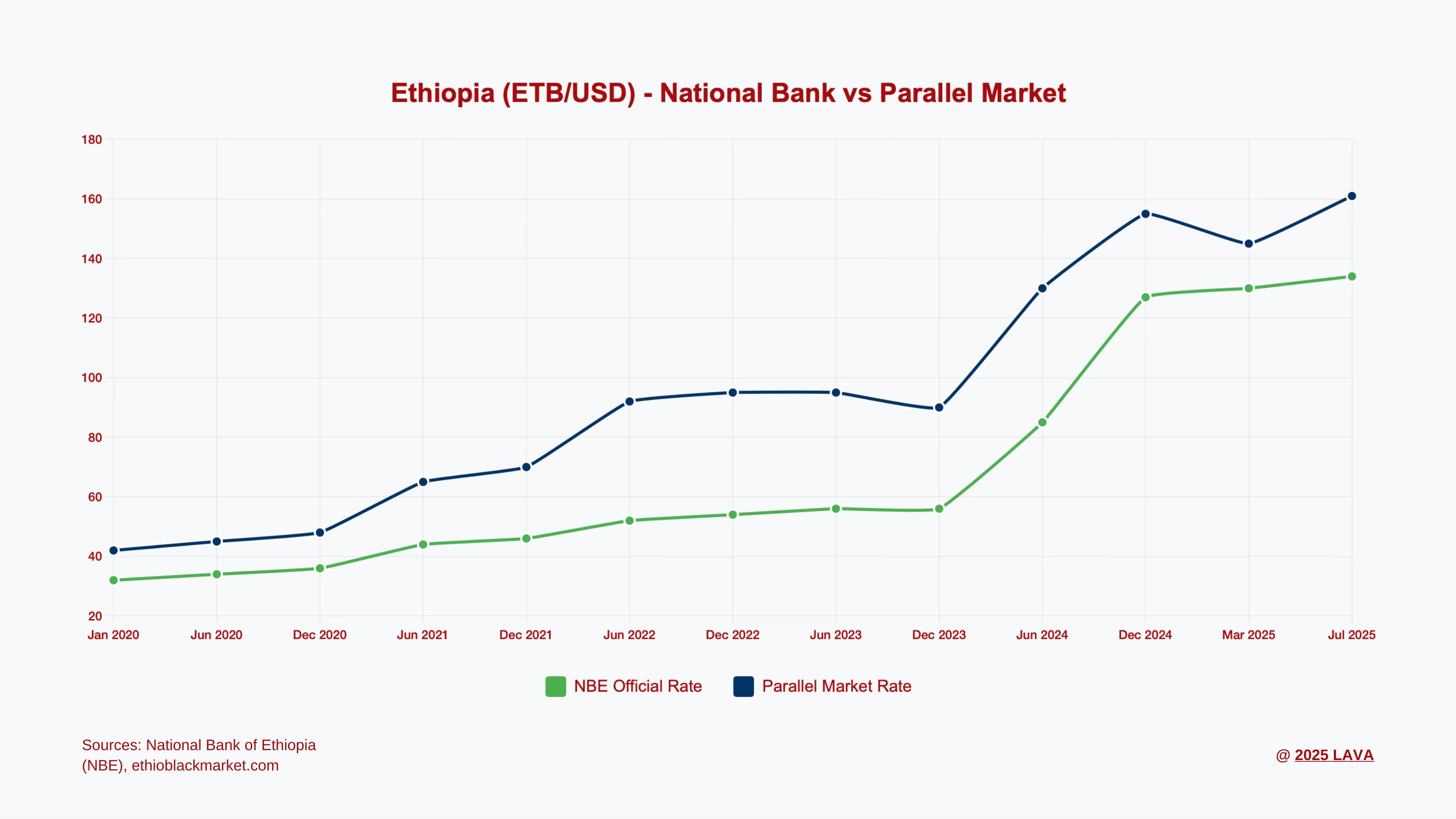

Ethiopia - Africa's second-largest country - has seen USD trade at 100%+ premium. The official rate stood at 55 Birr per $1, while open markets charged over 120 Birr. Import restrictions have affected essential commodities for years, and at certain points during the crisis the government made it illegal for Ethiopians to physically hold more than $3,000 USD. This continued until the National Bank of Ethiopia secured a substantial IMF loan in 2024, which will contribute to future debt and interest cycles.

These aren’t isolated cases: they represent a continent-wide crisis.

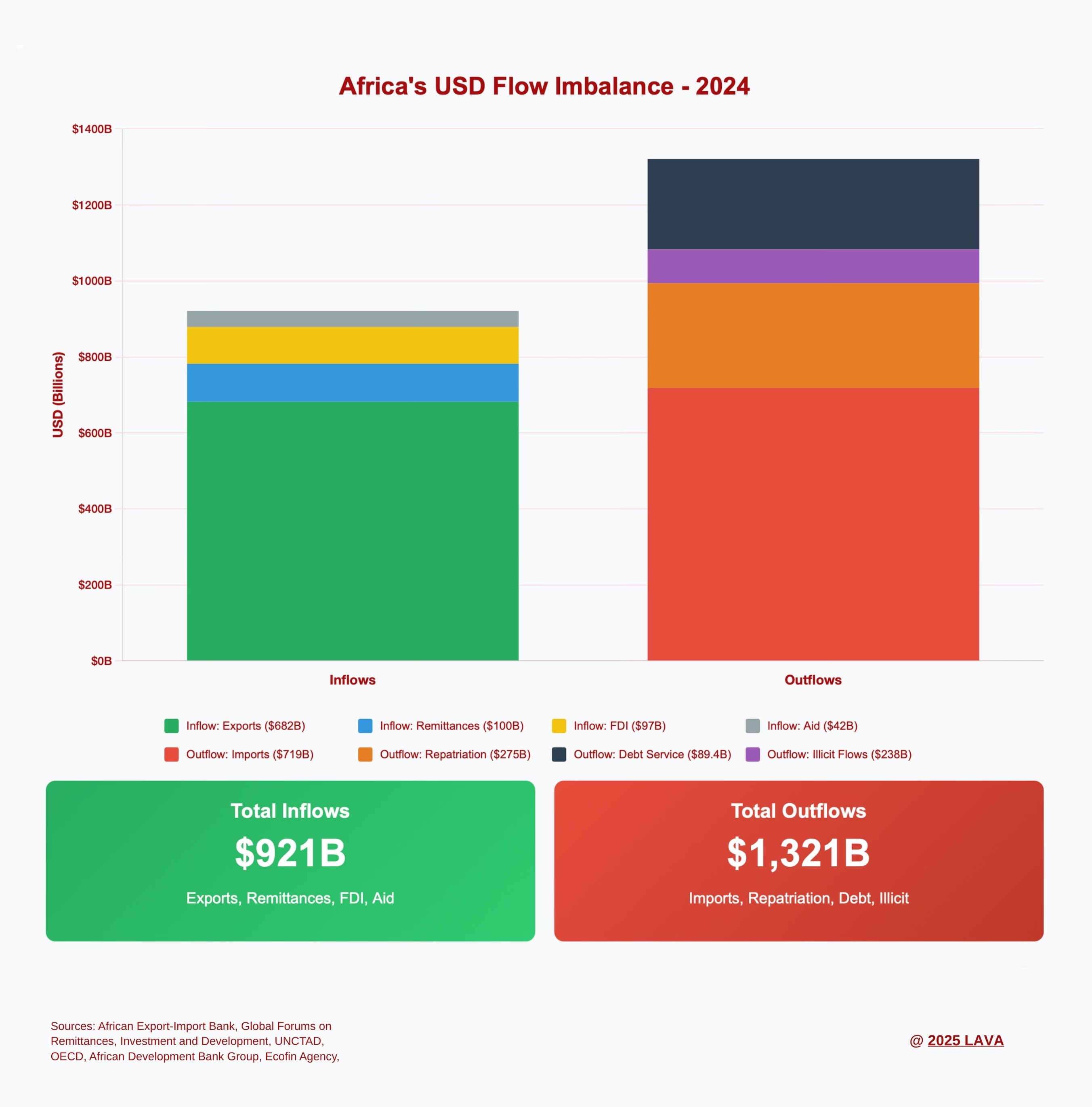

Africa faces a multi-decade USD shortage, driven by simple math: more dollars leave than enter.

Major inflows: export revenues ($682B in 2024), remittances (~$100B in 2024), Foreign Direct Investment ($97B in 2024), and development assistance aid ($42B in 2024. Major outflows: imports ($719B in 2024), multinational repatriation of proceeds ($275B estimate for 2022), external debt service ($89.4B in 2024), corruption and illicit flows ($238 Billion, according to the African Development Bank).

African debt has doubled over the last decade, alongside rising interest rates - 14.8% of export earnings serviced debt in 2023, from 4.5% in 2011. While exports are rising and GDPs are growing the fastest in the world, aggressive money printing by African governments devalues local currencies, reducing purchasing power and increasing USD demand. In Nigeria alone, the official USD price rose from 449 NGN (2022) to ~1,560 NGN (June 2025). COVID-era oil price hikes and economic slowdowns have further exacerbated these challenges.

The result? Systemic USD scarcity that forces even legitimate businesses into parallel USD markets.

The recurring pattern: when scarcity hits, governments implement stricter capital controls, resulting in banks rationing USD access. This creates a vicious cycle: the more controls are imposed, the more USD flows outside the banking system. Such a pattern affects everyone from retail users, SMEs, to large institutions.

Enter the parallel USD economy: Forex bureaus, Hawala networks, and informal traders became the primary USD distribution channels.

This parallel economy operates through a fragmented network: small Forex shops, or traditional businesses that run Forex services off the books, or even known individuals in communities. Some bureaus are regulated, many are not. Some are networked, such as the Hawala, who has developed internal communication channels across the world. These fragmented networks handle 90% of USD liquidity in countries like Nigeria. They are expensive, slow, and require high levels of trust.

Before USD stablecoins existed, the parallel USD economy was already normalized at a massive scale. Stablecoins simply digitized what was already happening.

Stablecoins solve for the liquidity fragmentation problem

The parallel economy services some USD liquidity needs, but is inefficient. When banks can't or won't provide USD access, businesses turn to alternative channels. A company that deposits $1M USD might wait weeks or months to withdraw it, forcing them into parallel markets that rely on trust networks, charge high fees, and involve manual processes.

USD stablecoins enable the emergence of coordinated marketplaces for this fragmented system. Many startups are already capitalizing on this opportunity.

A simplified explanation of how it works: instead of a person going to a physical Forex bureau with cash, or a business approaching multiple banks or Forex shops with large amounts of USD, they can now access aggregated liquidity through online stablecoin marketplaces and exchanges. Individuals/companies use their local currency or convert USD into stablecoins to provide liquidity to on/off ramp platforms, and earn yields while serving the other side of these more open marketplaces.

The impact is measurable: In 2024, $59B worth of crypto was transacted in Nigeria alone - equivalent to 31% of the country’s $188B nominal GDP (IMF). Across Sub-Saharan Africa, onchain transactions totalled $125B according to what Chainalysis was able to trace. We believe actual volume likely exceeds this significantly based on WhatsApp/Telegram activity, our portfolio data, and centralized exchange liquidity flows.

Most telling is how the USDT price on Binance’s P2P marketplace has been used as the reference rate for USD in Nigeria’s parallel market.

As a consequence, stablecoins offer the first large-scale USD liquidity coordination mechanism in Africa.

Mobile money laid the digital foundation

Sub-Saharan Africa processed $1.1 trillion in mobile money transactions in 2024 across 1.1 billion unique accounts and 165 live services.This creates three critical advantages for stablecoin adoption:

First, many Africans already trust digital money. After two decades of mobile money penetration, where in countries like Kenya more than half the economy runs on M-Pesa, users have learned that phone-based digital value is reliable and useful.

How does mobile money work? Telecommunications companies deposit cash in bank trust accounts, creating corresponding "digital float" for mobile service customers. Phone numbers become default 'bank accounts', with USSD messaging facilitating value exchange. Extensive "agent" networks–retailers, kiosks, and shops–provide cash-to-mobile money exchange services and share fee revenue.

Second, the infrastructure to move between fiat and stablecoins already exists. The capacity to do 24/7 settlements that appear within seconds (including for feature phones), and the ability to match a user’s registered name to that on the crypto marketplace, significantly reduce friction to settle fiat-stablecoin transactions instantaneously.

Third, the behavioral patterns are already established. Users are comfortable with digital-to-cash conversions, peer-to-peer transfers, and phone-based financial services.

Moving from mobile money to stablecoins requires minimal behavioral change - just switching from local digital currency to global digital currency. On/off ramping is possible without touching physical cash, and without those conducting the exchange needing to meet in person or go to a shop.

In countries like Nigeria, banks caught up with mobile money and leaned into mobile banking for 24/7 settlements within seconds. The same patterns of on/off ramps with mobile money are reflected with mobile banking.

Three waves of innovation brought stabelcoins mainstream

USD stablecoin adoption has moved beyond the parallel market and is eating into the banking sector at scale.

Wave 1: Basic exchange infrastructures. Early adopters used exchanges like Binance’s P2P marketplace, where merchants can process $5 to hundreds of thousands in USDT transactions. The Nigerian government claimed Binance processed $25B worth of crypto in 2024. Startups such as Luno, Quidax, BuyCoins, Valr, BitMama, Paxful, Ovex, and many others offered exchange services through central order books and P2P.

Whatsapp and Telegram OTC groups captured medium to large sized transactions, where buyers and sellers meet in closed groups and transactions are settled using escrows under supervision of the trusted group host.

Wave 2: fiat-to-stablecoin orchestration. Companies like HoneyCoin, KotaniPay, Busha, YellowCard, Fonbnk, and others built sophisticated APIs and fiat-stablecoin orchestration for businesses and retail consumers.

With companies like Bridge, combined with Circle and Tether mint facilities in the West, African startups are able to offer end-to-end services that integrate local fiat directly into global financial systems, all via stablecoins. To illustrate, HoneyCoin offers business clients USD denominated virtual bank accounts in the US / Europe, payment processing in 8+ African currencies (hosted by local banks), and manage their treasury in stablecoins.

Bridging traditional banking, parallel market liquidity, and USD stablecoins together, while serving non-crypto users has unlocked a significant share of the African market.

Almost all crypto products that interface with fiat have embedded KYC, AML, and additional compliance requirements, derisking it for larger institutions.

Wave 3: consumer wallets and embedded finance. Products like MiniPay serve millions of users through a browser-based interface, on the most used browser in Africa. Products like Onboard offer a consumer-tailored wallet with multiple apps for professionals and remote workers. Blockradar has created wallet infrastructure for Web2 fintech companies to offer USD accounts powered by stablecoins. Protocols like Paycrest and Accrue’s Cashramp automate fiat-crypto exchanges by pooling both sides of the liquidity market. There are many more innovations that are bringing core financial services directly to where users already are, including non-financial tools.

The results these waves? Cross border payments that cost 8%-20% through Western Union or Forex services now cost <1%. Settlement times have dropped from T+5 days to seconds for most transactions, or under a day for very large volumes that would normally take longer than a week. Fast settlements provide immediate working capital to users and protect them from currency devaluation risks that might happen during long wait periods. These value propositions are very attractive to all types of users who need to make cross-border payments.

Where are we going?

Based on patterns so far, here are a few speculations of where the USD stablecoin landscape could be in the next 3-5 years.

Bypassing SWIFT for global payments

With the structural advantages that stablecoins offer, we expect to see financial service providers to completely bypass SWIFT and traditional intermediaries entirely for certain payment types.

Stablecoin orchestrators like HoneyCoin and KotaniPay serve regulated Payment Service Providers to access stablecoins so they can offer more products to their customers (bypassing traditional rails). As greater regulatory clarity approaches, we expect more institutional adoption, and at a larger scale.

The global stablecoin infrastructure is getting more sophisticated and integrated into the global financial system (e.g. Visa, Mastercard, Stripe, the Genius Act, and the Hong Kong Stablecoin Bill), and liquidity flows between Africa and the rest of the world will keep getting more streamlined with less friction.

Regulatory clarity

African governments are creating clearer frameworks rather than fighting the market. South Africa was one of the first to regulate crypto assets and exchanges, which attracted a number of African companies to acquire licenses there. Nigeria, Kenya, Ghana, Mauritius, Rwanda, Seychelles, and many other countries are developing licensing frameworks and regulatory sandboxes. The overarching recognition is that crypto’s growth cannot be ignored.

The long-term dilemma for regulators to navigate is balancing capital controls, possible USD leakage through stablecoins, and growing their central banks’ Forex reserves. If USD access becomes frictionless, users would move their liquid assets to USD when their local currencies devalue fast, which can further exacerbate currency devaluation. Managing that well is going to put regulators to a test.

Product positioning

As on/off ramp and orchestration services become commoditized, we believe competitive advantages will concentrate around liquidity depth on each platform and distribution strength.

More liquidity means more competitive pricing, which attracts more users and drives even more liquidity onto the platform. While specialization in specific markets helps products get off the ground, we anticipate more aggregation of services, be it through company consolidations, product integrations, or companies building multiple products in-house. ‘’One-stop-shop” experiences that bring solutions together is a pattern we expect to see.

Products like Onbaord are showing us integrations of wallet + payment functionalities + issuance of debit cards to spend stablecoins + on/off ramp + invest / save, all on a single platform.

Global players and local advantage

Major players like Stripe, Coinbase, PayPal, Visa, and more who are betting on stablecoins still don’t have the rails to integrate the African market and its long-term potential.

As an example, Stripe’s stablecoin accounts cover 101 countries, but are missing all the critical African markets, including Nigeria, South Africa, Kenya, Ghana, Ethiopia, DRC, and Egypt: over 730 million people combined.

Local startups have a 3-5 year head start in integrating dozens of payment infrastructures, compliance requirements, user trust, and two sided liquidity access. For global companies seeking effective entry points into Africa, we expect partnerships or acquisitions will be more cost effective than starting from scratch.

Beyond USD: the next frontier

USD stablecoins solved Africa’s USD liquidity fragmentation and proved that blockchain-powered money can work at continental scale. But there isn’t evidence yet that they are solving for the USD flow imbalance - the fundamental problem African countries face. Still, $208 billion in intra-African trade routes through expensive USD intermediaries: a major problem that keeps depleting USD reserves for those countries, and ultimately affects the end users.

The next frontier of crypto innovation in Africa isn't just promulgating USD stablecoins, it's bringing African currencies onchain too.

Complete dollarization through stablecoins would be counterproductive. We think that would be a failure mode for crypto’s success in Africa long-term.

In Part II of this series, we explore how local currency stablecoins could unlock even greater efficiencies and actually tackle the USD flow imbalance, while preserving monetary sovereignty.

Special thanks to cryptowanderer and See Eun for feedback and review.

Looking forward to Part 2 mate! The data clearly indicates that local banks are going to take a heavy beating, not only on the plummeting USD deposit but also savings in local currencies.

Local stablecoins will solve the infrastructure issues most developing countries face but I don't see how they solve inflation (or arbitrary regulations like cash withdrawal limits) to make the currency more lucrative.

But how do ChainAnalysis and other institutions or organizations studying this phenomenon manage to measure the level of usage in a given country? Do they rely solely on IP addresses accessing APIs, and if so, how do they get access to the API data? Exchanges and stablecoin issuers probably don’t share that information